Pandora Stock: Great Business At A Fair Price (OTCMKTS:PANDY)

[ad_1]

MinttuFin/iStock via Getty Images

Introduction

Pandora A/S (OTCPK:PANDY) is a Danish jewelry company with affordable prices accessible to most people. A few years ago, the Pandora brand was taking an unclear direction. The current management team in 2018 launched a successful turn-around operation and relaunched the company’s image making Pandora the first jewelry brand recognized worldwide for its “modular” bracelets. To date Pandora has a formidable vertically integrated business with high margins, strong cash generation and an outstanding ROIC. The fears of the market have brought down the valuation and have reached interesting levels that in my opinion can offer an excellent risk/reward ratio.

Business

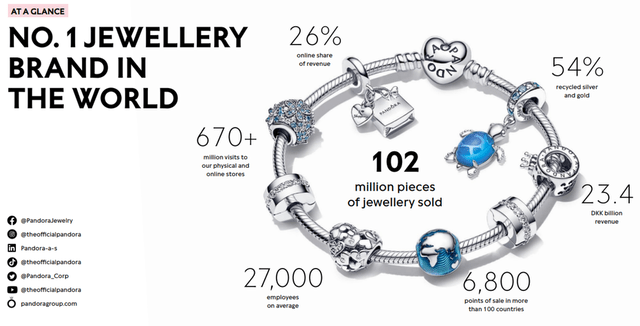

Pandora has a totally vertical integrated business model: from the study of product design to their production up to distribution through physical and online stores. In the past the brand had entered a negative spiral due to bad management policies, towards the end of 2018 a 2-year turn-around program called “Program NOW” was launched to put the company back on track. CEO Alexander Lacik and the entire board of directors, did an excellent job reducing the constant discounts that were put in place and making product offering easier and more productive. The Pandora brand today is stronger than ever, now they are ready to enter the third chapter of their history with the implementation of the “Phoenix Strategy” aimed at exploiting the strengths of the company and concentrated around 4 pillars: brand, design, customization and core markets.

Pandora Q1 22 Presentation

In 2021, 71% of the revenues was generated by Pandora Moments and Collabs, it is also the segment that allowed an impressive sell-out growth of 20%. The success of Pandora charms has also been impressive thanks to very profitable collaborations with Disney using the Star Wars and Marvel brands that have led many fans to queue outside Pandora stores and put themselves on waiting lists to be able to have the jewels of their favorite characters. The second major source of income is Pandora Timeless, which accounts for 17% of revenue in 2021 and achieved a sell-out growth of 19%. Also in 2021 Pandora also launched Pandora Brilliance, their first collection of lab-created diamonds, for now only in the UK but by the end of 2022 it should be available globally. To conclude, in September they launched Pandora ME which targets Generation Z and which in Q4 accounted for 4% of revenues.

As regards the distribution of revenues between the various sales channels, we find an important slice occupied by the online:

Pandora 21 Annual Report

Some previous articles on Pandora speculated that in the future the share of online sales could become increasingly important, making Pandora a predominantly online jewelry brand. The pandemic has undoubtedly influenced this type of sales but it does not seem to be the intention of the management to aim to make Pandora an e-commerce company. In recent months many franchise store chains have been purchased, such as the ones in North America and Portugal. The Phoenix strategy highlights how the growth of the Concept Stores is a fundamental point. For the purchase of jewelry many people prefer to go in person to try them on and see how they fit. Pandora’s online presence is still important and will not be abandoned but, in my opinion in this sector it is much more important to develop a network of stores in strategic points to guide the growth of the company.

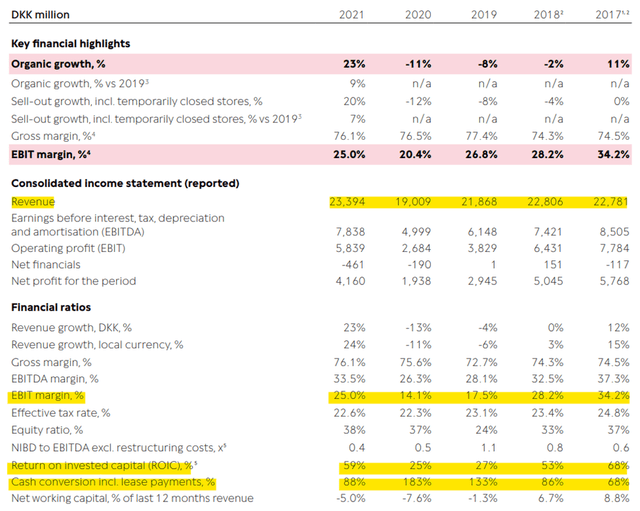

The Phoenix Strategy aims to double the revenues from the US compared to 2019 (DKK 4.7 billion) and to triple those from China again compared to 2019 (DKK 2 billion) in the long term. Store expansion is essential to achieving these ambitious goals and although investments in China have been postponed due to current unfavorable conditions I think Pandora’s products can be very successful in China. The management plans to invest DKK 1 billion to improve production capacity through a new production site in Vietnam that will be able to produce 60 million pieces annually, and expanding the current capacity of the factory in Thailand by an additional 20 million pieces. Overall we are talking about a 60% increase in production. The opening of the new crafting facilities is scheduled for 2023 in Thailand and for 2024 in Vietnam. In 2021, Pandora’s revenue amounted to DKK 23.39 billion, with organic growth of 9% compared to 2019 (+ 23% compared to 2020), an EBIT margin of 25% and a ROIC of 59%. Cash flow from operating activities of DKK 6.23 billion and Capex of DKK 641 million. The following tables show some important data of the last 5 years of Pandora, highlight the period of difficulty it has gone through and how they managed to get out of it. A point that I think is very important is free cash flow, which has remained consistent even in difficult times.

Pandora 21 Annual Report

Pandora 21 Annual Report

Latest Results

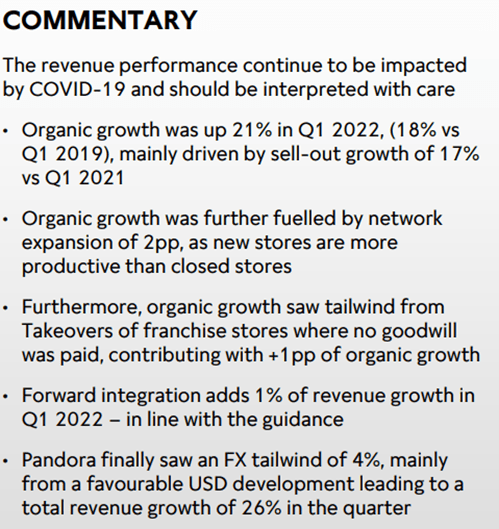

On May 4, 2022, Pandora published its first quarter results with excellent results.

Pandora Q1 22 Presentation

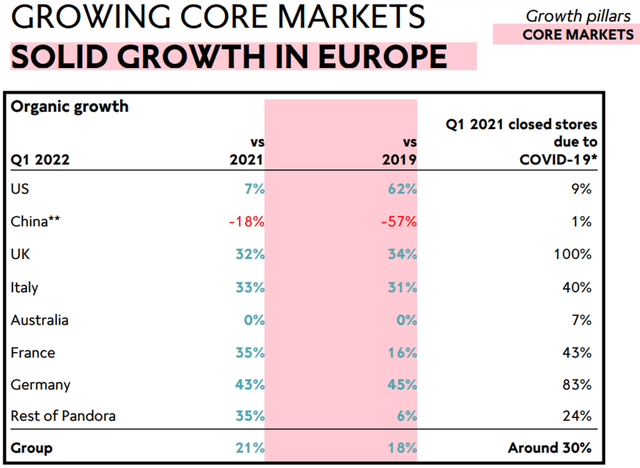

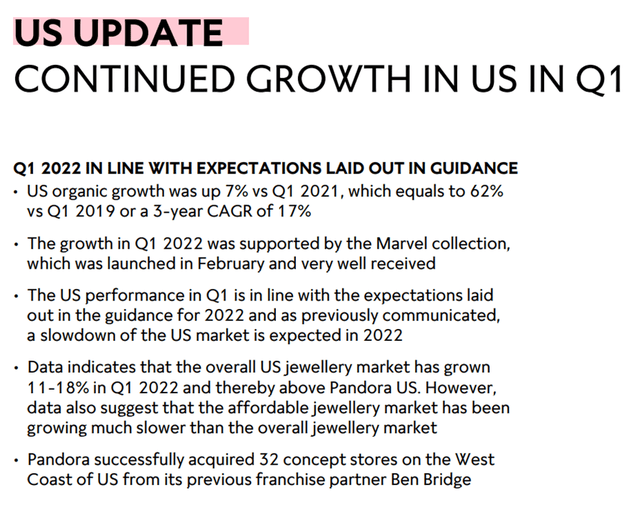

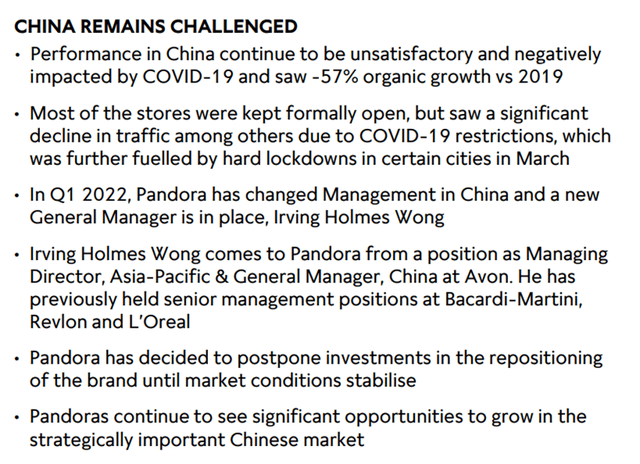

Growth was also favored by the reopening of many stores, in fact the reference quarter was characterized by the closure of many stores due to the restrictions for COVID-19. China was clearly the weakest market, as it was easy to imagine due to the no COVID policy implemented by the Chinese government. After a very strong 2021 in the USA, the first quarter of 2022 showed signs of a slowdown, but it is nevertheless interesting that revenues have still grown thanks to the Marvel collection. For the remainder of 2022 management expects a weaker market in the US.

Pandora Q1 2022 Presentation

Pandora Q1 2022 Presentation

Sales from online stores decreased by 17%, in 2021 they were driven by the closure of many stores (about 30%). This is a point in favor of the fact that people prefer to buy jewelry in physical stores rather than online, even though sales compared to 2019 have increased by 155%. Gross margin decreased slightly from 76.3% to 76% due to unfavorable changes in the commodities market and FX, lower discounts and a more favorable channel mix helped to keep the gross margin high. As for the EBIT margin, there was a significant improvement, going from 20.1% to 23% thanks to a strong operating leverage. To conclude, EPS and ROIC increased significantly thanks to the increase in revenues and operating leverage reaching EPS of DKK 10.5 (DKK 6.3 in Q1 2021) and a ROIC of 49% compared to 29% of the last year.

Pandora Q1 2022 Presentation

Valuation

For the valuation I will consider as usual three cases with different growth rates and multiples, trying to be conservative. For 2022 and 2023 I will look at analysts’ FCF estimates of DKK 4.7 billion and DKK 5.5 billion respectively.

- Base case: 2% CAGR up to 2031, FCF multiple: 15;

- Best case: CAGR 5% up to 2026 and 3% up to 2031, FCF multiple: 20;

- Worst case: no growth, FCF multiple: 10.

Looking back at previous years I have also estimated that 35% of the FCF will be returned to shareholders via dividends. Some buybacks have also been made over the years but I will not consider their effect in the valuation, but keep in mind that they could have a very important effect on the share price. I used a 10% discount rate and these are the results:

- Base case: DKK 52.94 billion

- Best case: DKK 74.58 billion

- Worst case: DKK 35.20 billion

The market capitalization of Pandora at the time of writing is around DKK 46 billion and by attributing probabilities to the three cases described (60% base case, 20% best and worst) we obtain an intrinsic value of DKK 53.72 billion, if we wanted to buy it with a margin of safety of 20% we should wait for it to reach 43 billion. I feel very comfortable with the estimates I have made because I think they are very reasonable if not too low. If management were able to execute the Phoenix strategy as it did between 2018 and 2021, the results could be much better. As for the risk/reward ratio, I think the numbers speak for themselves, at best we could triple the capital in 10 years, at worst we will get a small capital gain but in the meantime we will take substantial dividends. In the best case scenario the FCF in 2031 will be DKK 7,45 billion, with a FCF multiple of 20 the market cap. would be around DKK 144 billion, 3 times more than it is now.

Risks

The main risks in my opinion are the strong exposure to a single type of product and geographical diversification. The Moments and Collabs segment occupied 71% of revenue in 2021, in the first quarter of 2022 the percentage dropped to 66% but there is still a strong dependence on a single type of product. The danger of this kind of risk always depends on the type of product we are talking about. For example, Apple also depends a lot on the sale of iPhone but the product is exceptional and loved. Pandora charms are much loved and have been very successful for many years proving that they are not just a passing trend. The introduction of other types of jewelry will certainly help Pandora to reduce this risk.

As for geographical exposure, Pandora is well diversified but has a strong exposure in markets such as Italy (10% of revenue in 2021) which in this macroeconomic situation are the most fragile. Overall UK, France, Italy and Germany accounted for 34% of sales in 2021 and Europe in general could suffer a lot in the medium term. On the other side, Pandora’s revenue from China is only 5% and once the restrictive measures have ended and investments have begun, the growth of this market could compensate for the weakness of the others.

Competition in my opinion is a secondary risk and will not be one of Pandora’s main problems in the coming years. Although in jewelry we find very important and renowned brands such as Tiffany or Cartier, most of these sell very exclusive jewels. As for affordable jewelry Pandora is the most recognized brand globally and this is a competitive advantage that will allow the company not to suffer too much competition.

Conclusion

Pandora is a great business that has been through tough times but is well positioned to capture future growth opportunities. The strong globally recognized brand and the winning formula of charms as collectibles are assets that Pandora will be able to exploit to confirm its leadership position. My biggest business concerns stem from medium-term macroeconomic conditions, in a prolonged recession spending on non-essential items would be easily cut off by people and that would weigh on Pandora’s sales. By extending the time horizon, the current valuation is still very interesting and offers an excellent risk/reward ratio.

[ad_2]

Source link